Inventory Expansion and Market Rebalancing

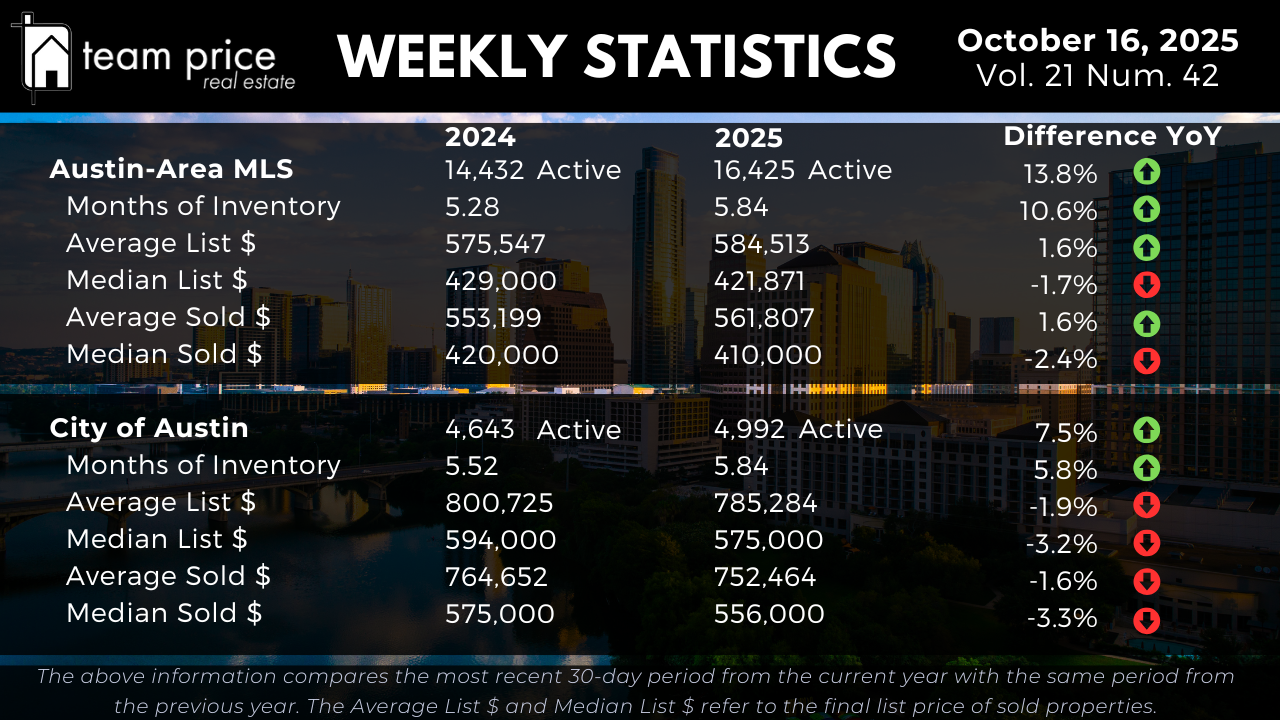

Inventory across the Austin housing market continues to expand through mid-October 2025, signaling a steady shift toward greater balance between buyers and sellers. The total number of active residential listings across the Austin-Area MLS has climbed 13.8% year over year, from 14,432 in 2024 to 16,425 this year. This sustained growth in available homes has pushed Months of Inventory up 10.6%, from 5.28 to 5.84 months, confirming that properties are taking longer to sell as absorption eases.

Inside the City of Austin, inventory growth remains more moderate but still meaningful. Active listings have increased 7.5% year over year, rising from 4,643 to 4,992, while Months of Inventory also ticked up from 5.52 to 5.84 months, a 5.8% gain. This increase is less dramatic than the broader metro area but continues the trend toward a slower-paced, more negotiable marketplace.

The overall takeaway: Austin’s housing market has officially entered its “balancing phase.” Buyers now have a wider selection of homes and stronger leverage during negotiations, while sellers must adapt pricing strategies to stay competitive in a market no longer defined by urgency.

Price Movement: Subtle but Directional

Price adjustments across the region remain modest, but directionally clear. Across the Austin-Area MLS, the average sold price rose 1.6% year over year, from $553,199 to $561,807, while the median sold price slipped 2.4%, from $420,000 to $410,000. These small shifts reinforce the picture of a market that is cooling without collapsing.

Among active listings, the average list price increased 1.6%, reaching $584,513, while the median list price declined 1.7% to $421,871. This divergence between mean and median reflects how higher-end properties continue to buoy overall averages, while median values reveal softening in the more affordable and mid-tier segments.

In the City of Austin, the pricing story is slightly more pronounced. The average list price declined 1.9%, from $800,725 to $785,284, and the median list price fell 3.2%, from $594,000 to $575,000. Closed sale prices show similar trends: the average sold price dropped 1.6%, from $764,652 to $752,464, while the median sold price fell 3.3%, from $575,000 to $556,000.

The city’s performance continues to underscore the bifurcation between suburban stability and urban correction. Outer-ring areas with newer construction and price diversity are holding firmer, while central Austin neighborhoods—particularly those dependent on move-up or discretionary buyers—are experiencing slightly more pricing pressure.

Negotiation Trends and Buyer Advantage

Negotiation continues to define the fall 2025 housing market. As of this week, 69.2% of closed sales have occurred below list price, up from 65.9% last month. Only 18.4% of homes sold at list price, and 12.4% sold above asking, marking a noticeable departure from the market dynamics of 2021–2022, when multiple offers and escalation clauses were the norm.

The average sold-to-list price ratio now stands at 97.15%, reflecting the consistent reality that sellers are conceding roughly 3% off original asking prices to secure contracts. For buyers, this means there is real negotiating room—especially on properties that have been on the market longer or received recent price reductions. For sellers, it underscores the importance of accurate pricing at launch; listings that come out too aggressively are often punished by extended days on market and steeper eventual discounts.

Regional and ZIP Code Performance

Across the 30 tracked cities in Central Texas, market performance remains diverse. 16 cities (53%) posted month-over-month price increases, while 14 (47%) recorded declines—a nearly even split that highlights localized resilience. On a year-over-year basis, 11 cities (37%) showed price gains, while 19 (63%) experienced declines.

At the ZIP code level, the picture is similar: 40 of 75 ZIP codes (53%) saw month-over-month price gains, while 33 (44%) reported declines. Year over year, 33 ZIPs (44%) posted gains, with 42 (56%) down. These ratios indicate a market that’s fragmented but trending stable—where micro-locations, school districts, and product type dictate outcomes more than broad regional momentum.

Only one ZIP code across Central Texas remains above its 12-month peak, while 74 ZIP codes are trading below their highs, confirming that Austin’s pandemic-era surges have fully corrected to sustainable, post-peak levels.

This localized dispersion is precisely what defines a mature market. Areas with strong job centers, limited new construction, or solid resale demand—such as Georgetown, Dripping Springs, and select corridors in Cedar Park—are maintaining stability. In contrast, higher-supply zones, particularly those dominated by new suburban development, continue to experience mild price drift and extended marketing times.

Prices Relative to Peak Levels

Relative to the market highs reached between 2022 and 2023, today’s pricing remains well below peak but largely stable year to date. Across the Austin-Area MLS, the average list price is down 9.3% from its March 2023 peak, and the median list price sits 17.7% below its May 2022 high. Similarly, the average sold price is 8.8% below peak, and the median sold price is 19.1% lower.

Inside the City of Austin, the numbers show slightly steeper historical adjustments. The average sold price is 6.3% below its May 2022 high, and the median sold price has fallen 16.3% from its peak. On a per-square-foot basis, both average and median values remain 20–26% below 2022 highs, suggesting that while price corrections have been significant, they have also largely stabilized.

These figures reinforce that Austin’s market has transitioned from rapid contraction into equilibrium. The volatility of 2022 has given way to steadier, data-driven fundamentals—a sign of a healthy, functioning market recalibration.

Market Outlook

As of mid-October 2025, the Austin real estate market stands at a crossroads of opportunity and caution. Inventory levels remain elevated, absorption is slower, and most transactions are closing below original list prices. Yet despite these headwinds, price stability and sustained buyer demand indicate that the market has found its footing after two years of adjustment.

For buyers, this is one of the most favorable environments in recent memory—ample selection, reasonable pricing, and motivated sellers. For sellers, success depends on preparation, presentation, and precision: accurate pricing, proactive adjustments, and realistic expectations are critical. For investors, today’s conditions present a long-term entry window, with most segments priced 15–25% below peak levels, creating solid fundamentals for appreciation once market velocity returns.

The Austin housing market in Q4 2025 is defined not by extremes, but by balance—a steady rhythm between supply and demand, patience and opportunity, discipline and optimism.